July 4, 2026

S&P 500 Drawdowns Since 1871: Every Decline, How Long They Lasted, and What Actually Recovered

Share on

What this is: every S&P 500 decline of 10% or more since 1871 (all 32 of them), computed from the raw index data, measured three honest ways, with the full table free to download. Historical measurement, not investment advice.

Contents

Markets fall. That's the deal.

What a drawdown is

How the numbers were built

150 years underwater

Every S&P 500 drawdown since 1871

How long do drawdowns last?

The 25-year myth and the hidden 1970s

The modern era: 2020, 2022, 2025, and 2026

What happened after the worst moments

The cost of panicking, computed

Japan, the UK, and survivorship bias

Key takeaways and FAQ

Markets fall. That's the deal.

As I write this, with data through July 2, 2026, the S&P 500 sits at or near an all-time high. It doesn't feel that way to most people who own stocks. The index dodged an official correction in March 2026, but the average S&P 500 member fell about 21% from its own high at some point this year, according to Charles Schwab's 2026 mid-year outlook. The headline number looked calm while most of the stocks inside it were getting beaten up. So people are asking the old questions again. How bad do declines get? How long do they last? Does the money actually come back?

This page answers those questions with a complete count rather than vibes. We took the S&P 500's full recorded history, back to January 1871, and extracted every decline of 10% or more. There are 32. For each one we measured how deep it went, how long the fall took, and how long the climb back took — and we did it three different ways, because the standard way of measuring (price only, ignoring dividends and inflation) turns out to distort the two questions people care about most.

Here's the single most useful fact in the whole study, up front: since 1871, the market has spent 82% of all months below some previous high. Being down is not the exception. It is the normal operating condition of owning stocks, and a 10% decline has arrived about every 4.9 years on average. If you internalize that one idea, everything below is detail.

What a drawdown is

Picture the market's chart as a rollercoaster track, but one that climbs over time. Every so often the track hits a new highest point. Then it drops, rattles around below that mark for a while, and eventually climbs past it to set a new record.

A drawdown is that whole round trip: the slide from a record high (the peak) down to the lowest point of the decline (the trough), then the climb back until the market closes above the old record (the recovery). The depth is the percentage lost from peak to trough. The whole time the market is below its old record, we say it is underwater.

One concrete example. On February 19, 2020, the S&P 500 set a record. COVID hit, and 33 days later it had lost 33.9% of its value, the fastest deep decline in the dataset. Then it turned. It took 148 more days to climb back above the February peak, which it did on August 18, 2020. Depth: −33.9%. Time underwater: 181 days, about six months, start to finish.

Why measure drawdowns instead of just returns? Because drawdowns are what you actually live through. An average annual return tells you nothing about the two years in the middle where your account was down 40% and you had to decide, every single day, not to sell. Depth and duration are the emotional load of investing, quantified.

How the numbers were built

Everything on this page comes from one reproducible computation. Here is the whole method, in plain terms:

Data, 1871–1927: Robert Shiller's public S&P Composite dataset, monthly, from January 1871 (1,866 months of prices, dividends, and inflation data through June 2026). One honest caveat: Shiller's monthly prices are the average of each month's daily closes, which smooths out fast crashes and makes early declines look slightly shallower and slower than they felt.

Data, 1928 onward: daily index closes (Yahoo Finance, ^GSPC), January 3, 1928 through July 2, 2026 (24,741 trading sessions).

What counts as an episode: every decline of 10% or more from a record high, measured on closing prices. That yields 32 episodes.

Lens 1 — Price: the index level alone, dividends ignored. This is what every chart on TV shows.

Lens 2 — Total return (TR): what an investor who reinvested every dividend actually experienced.

Lens 3 — Real total return: total return adjusted for inflation, meaning what your money could actually buy.

The three lenses matter because they disagree, badly, about the biggest question in market history. Section 7 shows how badly. And the monthly-averaging caveat is not hypothetical: the 1929–1932 collapse measures −84.76% on monthly-average prices but −86.2% on daily closes. Fast crashes lose some of their violence when you average them.

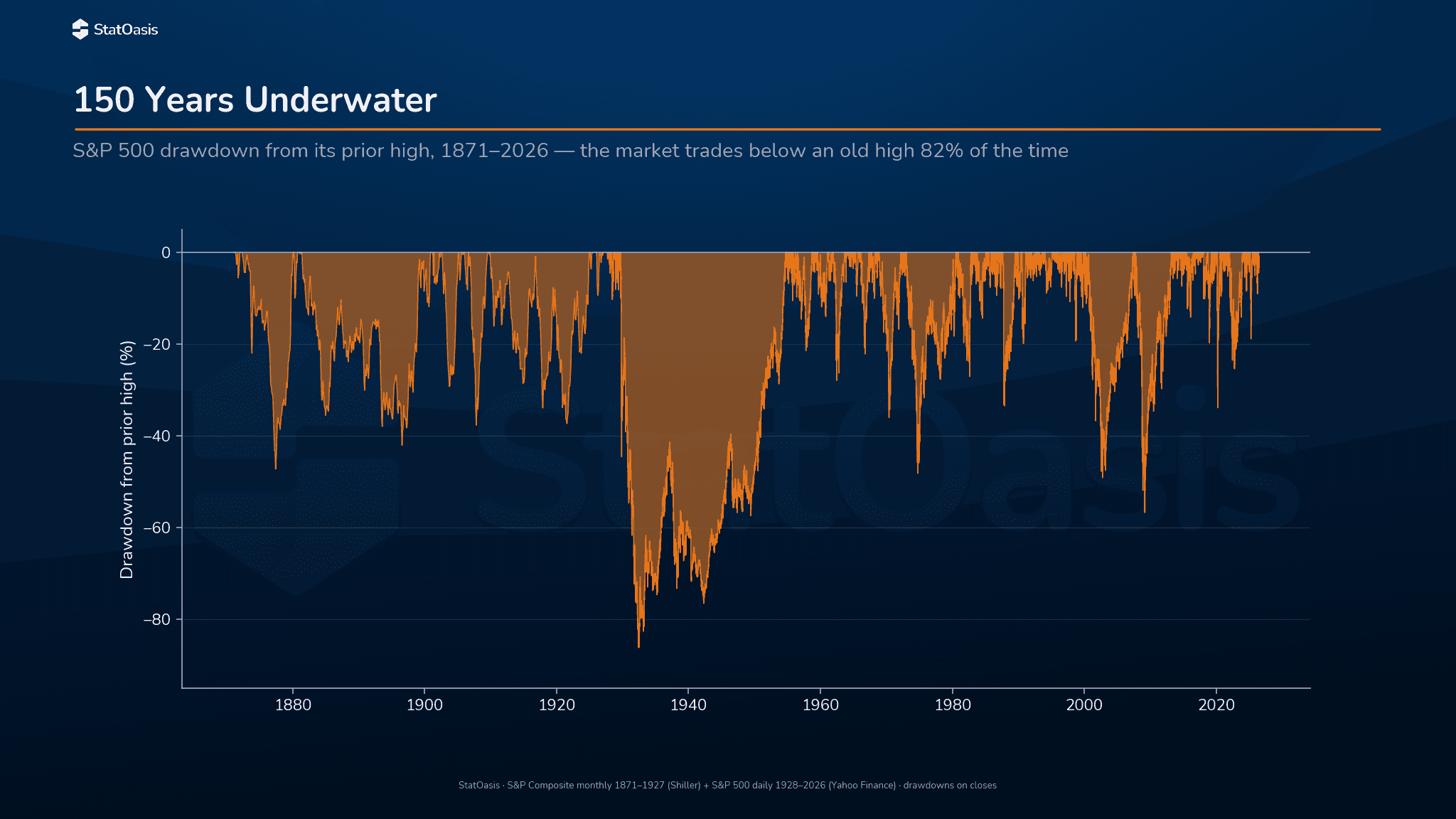

150 years underwater

This is the study's hero chart: the S&P 500's distance below its record high, every month from 1871 to 2026. You'll recognize the spikes by name (1929, 1973, 2000, 2008), but look at how little of the chart sits on the zero line.

150 years underwater: the market's distance below its record high, 1871–2026. The zero line — a fresh all-time high — is the rare event. Source: StatOasis, computed from Shiller monthly + daily S&P 500 data.

Counted month by month on the price lens, the market was at a new high in only 18.0% of all months since 1871. It spent 82.0% of months below a prior peak, 55.8% of months in a drawdown of at least 10%, 35.1% in a drawdown of at least 20%, and 21.2%, one month in five, down 30% or more from its high.

Dividends soften this picture considerably. Count the same months on total return and the market was at a high 31.0% of the time, with only 31.0% of months in a 10%-plus drawdown. Adjust for inflation and it lands between: at a high 24.4% of months, in a 10%-plus real drawdown 42.0% of the time.

Lens | Months at a high | Months below a high | In a ≥10% drawdown | In a ≥20% drawdown | In a ≥30% drawdown |

|---|---|---|---|---|---|

Price only | 18.0% | 82.0% | 55.8% | 35.1% | 21.2% |

Dividends reinvested | 31.0% | 69.0% | 31.0% | 14.6% | 9.2% |

Dividends + inflation-adjusted | 24.4% | 75.6% | 42.0% | 26.2% | 14.0% |

Whichever lens you prefer, the conclusion holds. An investor who feels uneasy whenever the market is below its old high has signed up to feel uneasy for most of their investing life. The high is the anomaly.

Every S&P 500 drawdown since 1871

Here is the complete record: all 32 declines of 10% or more, sorted by when they started. Rows marked † come from the monthly-average era (before 1928), so their dates are month-precision and their depths are slightly smoothed.

Peak | Trough | New high | Depth | Days falling | Days recovering | Years underwater |

|---|---|---|---|---|---|---|

1872-05-01 † | 1877-06-01 | 1880-02-01 | −47.3% | 1,857 | 975 | 7.8 |

1880-03-01 † | 1880-05-01 | 1880-10-01 | −10.0% | 61 | 153 | 0.6 |

1881-06-01 † | 1896-08-01 | 1900-12-01 | −42.1% | 5,540 | 1,582 | 19.5 |

1902-09-01 † | 1903-10-01 | 1905-03-01 | −29.3% | 395 | 517 | 2.5 |

1906-09-01 † | 1907-11-01 | 1909-08-01 | −37.7% | 426 | 639 | 2.9 |

1909-12-01 † | 1921-08-01 | 1925-01-01 | −37.4% | 4,261 | 1,249 | 15.1 |

1928-05-14 | 1928-06-12 | 1928-08-28 | −10.3% | 29 | 77 | 0.3 |

1929-09-16 | 1932-06-01 | 1954-09-22 | −86.2% | 989 | 8,148 | 25.0 |

1955-09-23 | 1955-10-11 | 1955-11-14 | −10.6% | 18 | 34 | 0.1 |

1956-08-03 | 1957-10-22 | 1958-09-24 | −21.5% | 445 | 337 | 2.1 |

1959-08-03 | 1960-10-25 | 1961-01-27 | −14.0% | 449 | 94 | 1.5 |

1961-12-12 | 1962-06-26 | 1963-09-03 | −28.0% | 196 | 434 | 1.7 |

1966-02-09 | 1966-10-07 | 1967-05-04 | −22.2% | 240 | 209 | 1.2 |

1967-09-25 | 1968-03-05 | 1968-04-29 | −10.1% | 162 | 55 | 0.6 |

1968-11-29 | 1970-05-26 | 1972-03-06 | −36.1% | 543 | 650 | 3.3 |

1973-01-11 | 1974-10-03 | 1980-07-17 | −48.2% | 630 | 2,114 | 7.5 |

1980-11-28 | 1982-08-12 | 1982-11-03 | −27.1% | 622 | 83 | 1.9 |

1983-10-10 | 1984-07-24 | 1985-01-21 | −14.4% | 288 | 181 | 1.3 |

1987-08-25 | 1987-12-04 | 1989-07-26 | −33.5% | 101 | 600 | 1.9 |

1989-10-09 | 1990-01-30 | 1990-05-29 | −10.2% | 113 | 119 | 0.6 |

1990-07-16 | 1990-10-11 | 1991-02-13 | −19.9% | 87 | 125 | 0.6 |

1997-10-07 | 1997-10-27 | 1997-12-05 | −10.8% | 20 | 39 | 0.2 |

1998-07-17 | 1998-08-31 | 1998-11-23 | −19.3% | 45 | 84 | 0.4 |

1999-07-16 | 1999-10-15 | 1999-11-16 | −12.1% | 91 | 32 | 0.3 |

2000-03-24 | 2002-10-09 | 2007-05-30 | −49.1% | 929 | 1,694 | 7.2 |

2007-10-09 | 2009-03-09 | 2013-03-28 | −56.8% | 517 | 1,480 | 5.5 |

2015-05-21 | 2016-02-11 | 2016-07-11 | −14.2% | 266 | 151 | 1.1 |

2018-01-26 | 2018-02-08 | 2018-08-24 | −10.2% | 13 | 197 | 0.6 |

2018-09-20 | 2018-12-24 | 2019-04-23 | −19.8% | 95 | 120 | 0.6 |

2020-02-19 | 2020-03-23 | 2020-08-18 | −33.9% | 33 | 148 | 0.5 |

2022-01-03 | 2022-10-12 | 2024-01-19 | −25.4% | 282 | 464 | 2.0 |

2025-02-19 | 2025-04-08 | 2025-06-27 | −18.9% | 48 | 80 | 0.4 |

† Monthly-average data (Shiller). All dates are the close-basis peak, trough, and first new high. Days are calendar days.

Download the full table as CSV. It is the exact file the charts and stats on this page are computed from.

A few things worth pulling out of the table. The deepest decline ever is 1929's −86.2%, and it also holds the record for time underwater: 25.0 years on a price basis (section 7 has a lot more to say about that number). The second-longest is one almost nobody talks about: the peak of June 1881 wasn't surpassed for good until December 1900, 19.5 years later. The fastest fall in the table is 2018's 13-day, −10.2% air pocket, and the most violent single day belongs to 1987: most of that year's −33.5% decline landed in one October session, Black Monday. (The fastest deep decline remains 2020's 33-day, −33.9% collapse.)

How long do drawdowns last?

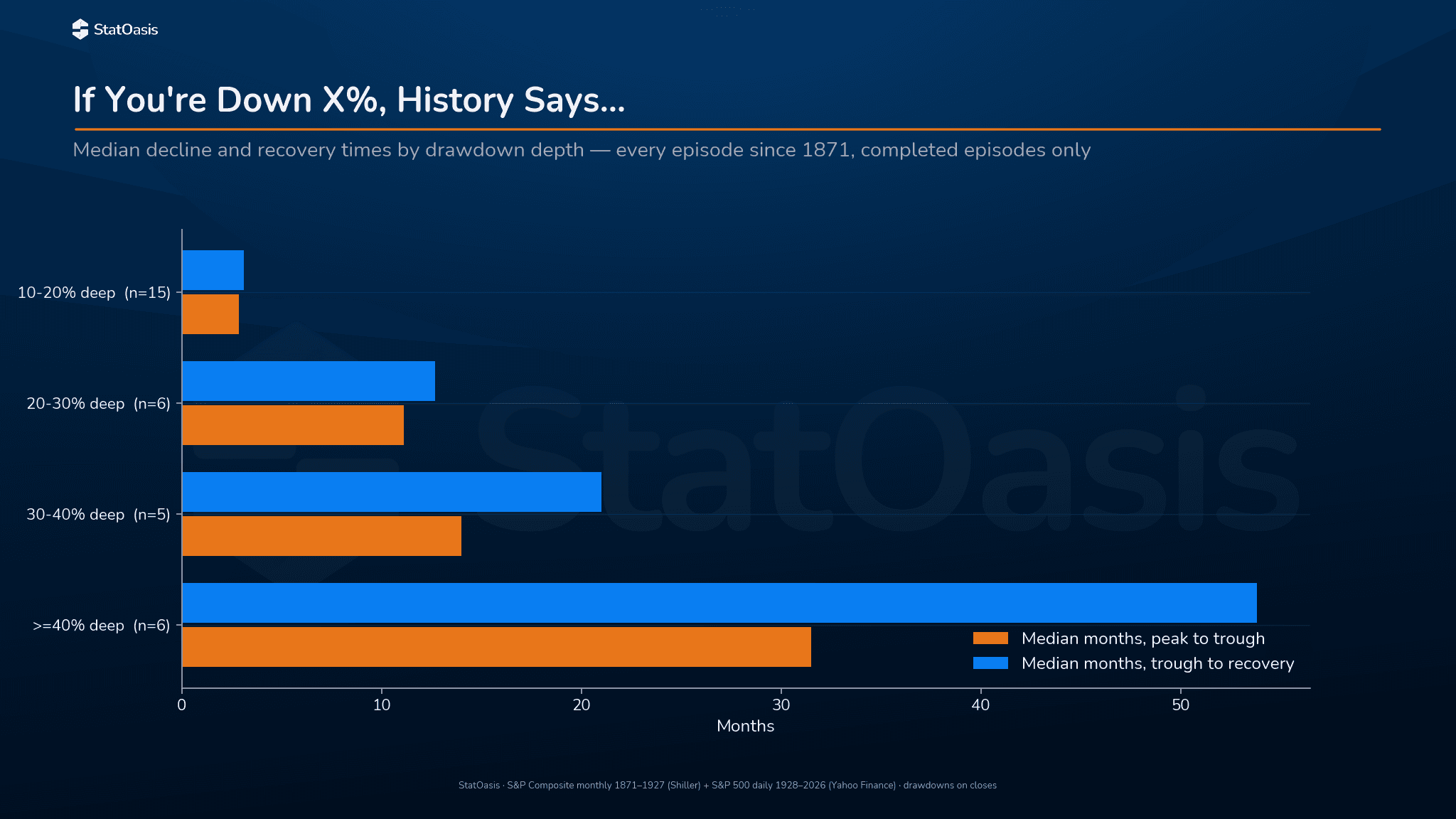

This is the question a scared investor actually wants answered, so let's answer it the way history allows: as a lookup table. Take every completed episode since 1871, group by how deep it went, and read off the median times. (The median is the middle value — half of the episodes were faster, half slower.)

Depth of decline | Episodes | Median days, peak to trough | Median days, trough back to the old high |

|---|---|---|---|

10–20% | 15 | 87 | 94 |

20–30% | 6 | 338 | 386 |

30–40% | 5 | 426 | 639 |

40% or more | 6 | 959 | 1,638 |

If you're down X%, history says: median peak-to-trough and trough-to-recovery times by depth, all completed episodes since 1871. Source: StatOasis, computed from Shiller monthly + daily S&P 500 data.

Read it as a rough map, not a schedule. A garden-variety correction (10–20%) has typically been a three-month fall and a three-month climb. Unpleasant, then over. A bear market in the 20–30% range has typically taken about a year to decline and a year to recover. The monsters, 40% and beyond, are a different animal: a median of 959 days falling and 1,638 days — roughly four and a half years — climbing back. Note the sample sizes, though. Six episodes is thin evidence, and your particular crisis is under no obligation to be median.

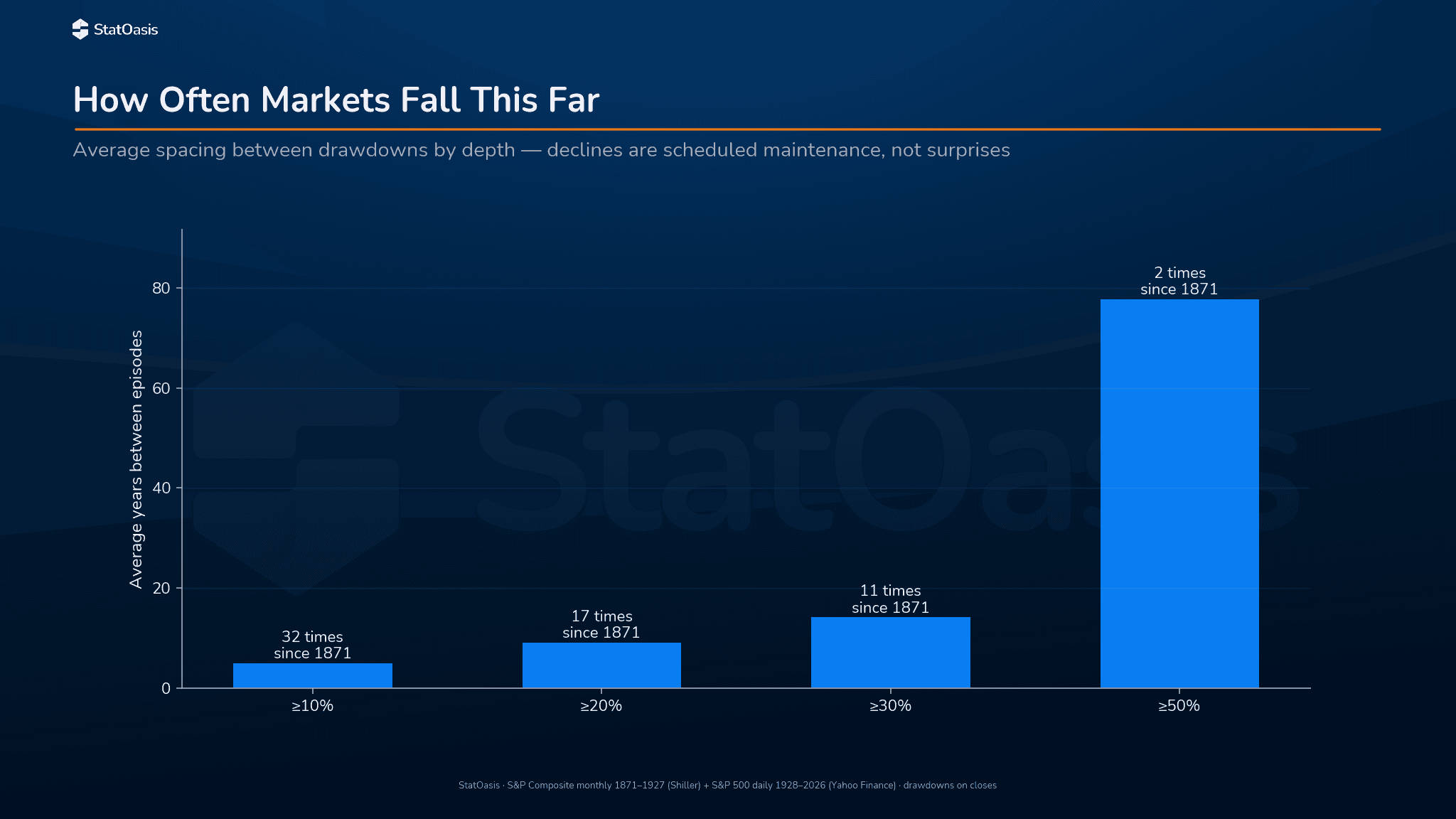

How often does each kind arrive? Since 1871:

Depth reached | Times it happened | Average years between |

|---|---|---|

10% or more | 32 | 4.9 |

20% or more | 17 | 9.1 |

30% or more | 11 | 14.1 |

50% or more | 2 | 77.7 |

How often markets fall this far: a 10% decline about every 5 years, a 20% bear market about every 9, a 30%+ crash about every 14. Source: StatOasis, computed from Shiller monthly + daily S&P 500 data.

A 10% decline roughly every five years. A 20% bear market roughly every nine. A 30% crash roughly every fourteen. These are not black swans; they're scheduled maintenance with an unpublished schedule.

One more pattern hides in the durations: recoveries have been getting faster. Take every episode of 15% or deeper and split the record at 1950. The six early episodes took a median of 1,112 days to recover. The fifteen years since 1950: 337 days. Modern markets are more diversified and more liquid, and central banks act faster, all of which has shortened the climb back. Though 1973 and 2000 prove "shorter" is not "short."

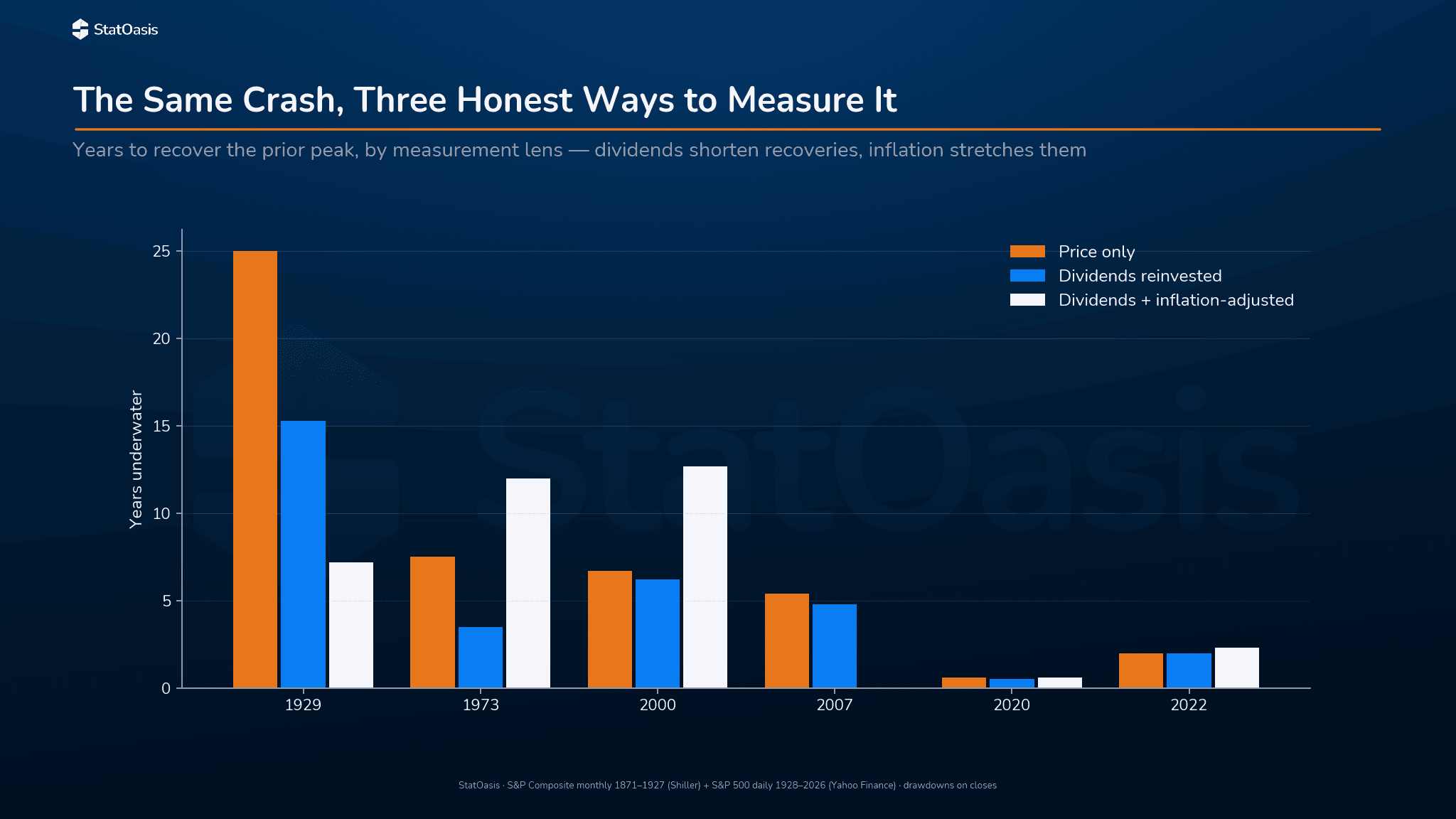

The 25-year myth and the hidden 1970s

You have probably heard the scariest statistic in investing: after the 1929 crash, the market took 25 years to recover. It's the number that launched a thousand "stocks are a casino" arguments. It is technically true and profoundly misleading, because it measures the index price alone — no dividends, no inflation. Nobody lived that number. So we measured every major crisis three ways.

Crisis (peak) | Price only | Dividends reinvested | Dividends + inflation-adjusted |

|---|---|---|---|

1929 | −84.76%, 25.0 yrs | −81.76%, 15.3 yrs | −76.8%, 7.2 yrs |

1973 | −43.35%, 7.5 yrs | −39.16%, 3.5 yrs | −50.06%, 12.0 yrs |

2000 | −43.65%, 6.7 yrs | −41.56%, 6.2 yrs | −51.76%, 12.7 yrs |

2007 | −50.82%, 5.4 yrs | −49.04%, 4.8 yrs | (no separate real-terms episode — see below) |

2020 | −19.09%, 0.6 yrs | −18.92%, 0.5 yrs | −18.86%, 0.6 yrs |

2022 | −20.29%, 2.0 yrs | −19.26%, 2.0 yrs | −24.5%, 2.3 yrs |

Monthly resolution (Shiller monthly averages), which is why 2020 shows about −19% here versus −33.9% on daily closes — monthly averaging smooths fast crashes, exactly the caveat from the methodology box.

Start with 1929. On price alone, an investor at the September 1929 peak waited until September 1954: the famous 25 years. But that investor was collecting dividends the whole time, and dividend yields in the 1930s were enormous precisely because prices had collapsed. Reinvest them, and the wait drops to 15.3 years. Now account for the deflation of the early 1930s — every dollar bought more — and in real purchasing-power terms, the 1929 investor was whole by November 1936. Seven point two years. Brutal, but a third of the legend.

Then the lenses flip on you. The 1973–74 bear looks moderate on price: down 43.35%, recovered in 7.5 years. But the 1970s ran on double-digit inflation, which price charts ignore. In real terms, the damage was −50.06% and the recovery took 12.0 years, until January 1985. The same trap hides in 2000: 6.7 years on price, but 12.7 years — until May 2013 — in real terms.

The same crash, three honest ways to measure it. Note 2007 shows only two bars: in real total-return terms, the market never climbed back above its 2000 peak before the 2008 crash hit, so the entire 2000–2013 stretch is one long real-terms drawdown with no separate 2007 episode. Source: StatOasis, computed from Shiller monthly + daily S&P 500 data.

That missing 2007 bar is worth sitting with. Measured in what your money could buy, with dividends reinvested, an investor at the 2000 peak did not get back to even until May 2013. The dot-com bust and the global financial crisis were one 12.7-year episode, not two. Price charts drew two valleys; a real investor lived one.

The honest summary of the three lenses: dividends make deep-crash recoveries much faster than the famous numbers, and inflation makes "mild" eras like the 1970s much worse. Any drawdown table that shows you only price — which is nearly all of them — is systematically wrong in both directions.

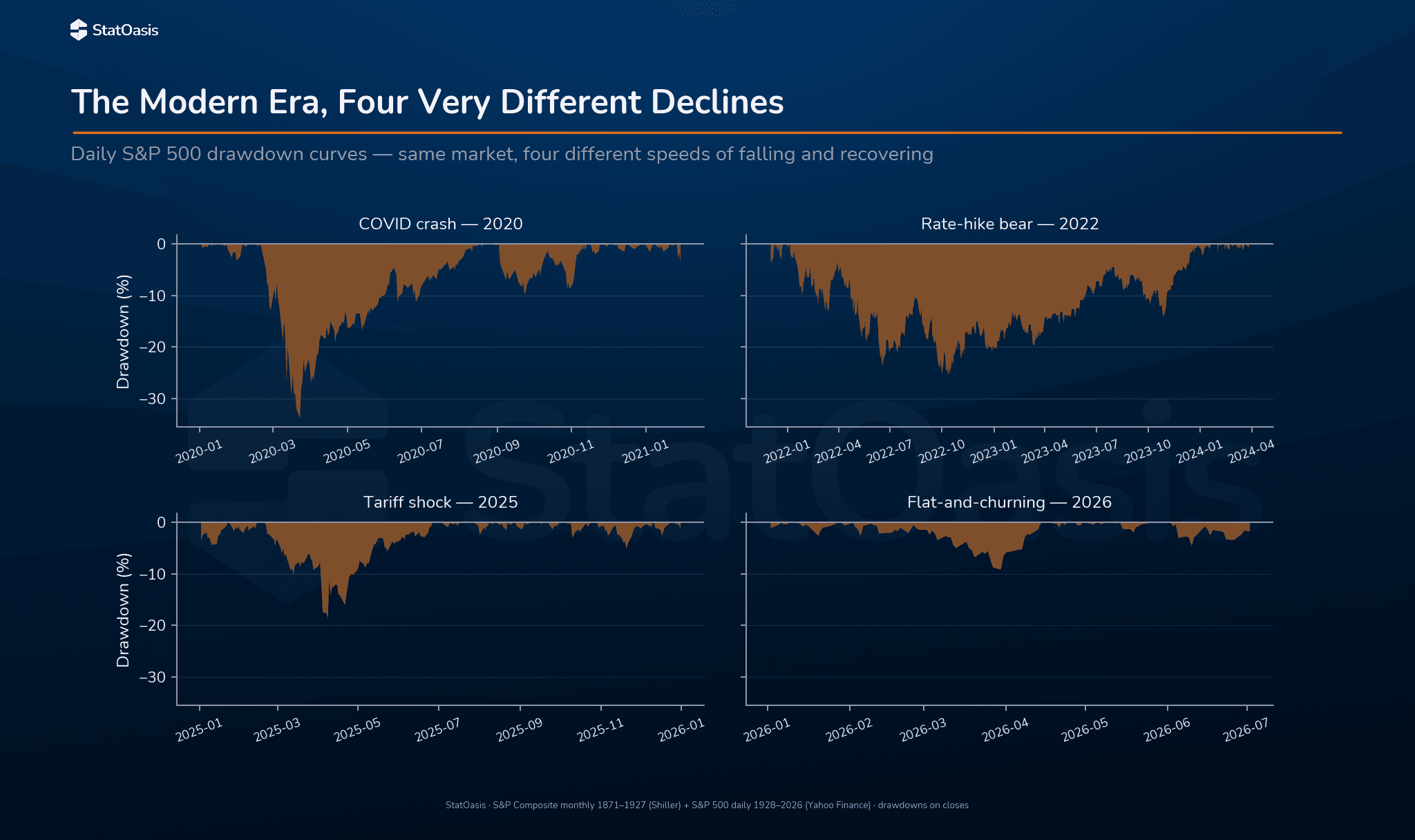

The modern era: 2020, 2022, 2025, and 2026

The last six years compressed a remarkable amount of drawdown history into a short window, and no two episodes looked alike.

Four very different declines: 2020's vertical drop and V-recovery, 2022's slow grind, 2025's sharp-but-brief tariff shock, and 2026's calm index. Source: StatOasis, computed from daily S&P 500 data.

2020 was the sprint: −33.9% in 33 days, then a new high 148 days after the bottom. Total time underwater, 181 days. An investor who blinked missed the whole thing; an investor who sold near the March low locked in the fastest self-inflicted loss in the table.

2022 was the grind: a 282-day slide to −25.4% as rates rose, then a 464-day climb. Two full years underwater, with no single dramatic day to point to. Grinds are harder on discipline than crashes, because there's never an obvious moment of capitulation to rally from.

2025 was the shock: the tariff announcements took the index down 18.9% in 48 days, just shy of the official bear-market line, and then it was over, with a new high 80 days later. Start to finish, 128 days.

2026, so far, is the strangest of the four: nothing, officially. No 10% episode through July 2. But per Schwab's mid-year outlook, the average index member fell about 21% from its own high during the year while the index avoided even a 10% correction in March. A calm index hid a member-level bear market — a good reminder that the S&P 500 is a weighted average, and the average can be serene while most of its parts are not.

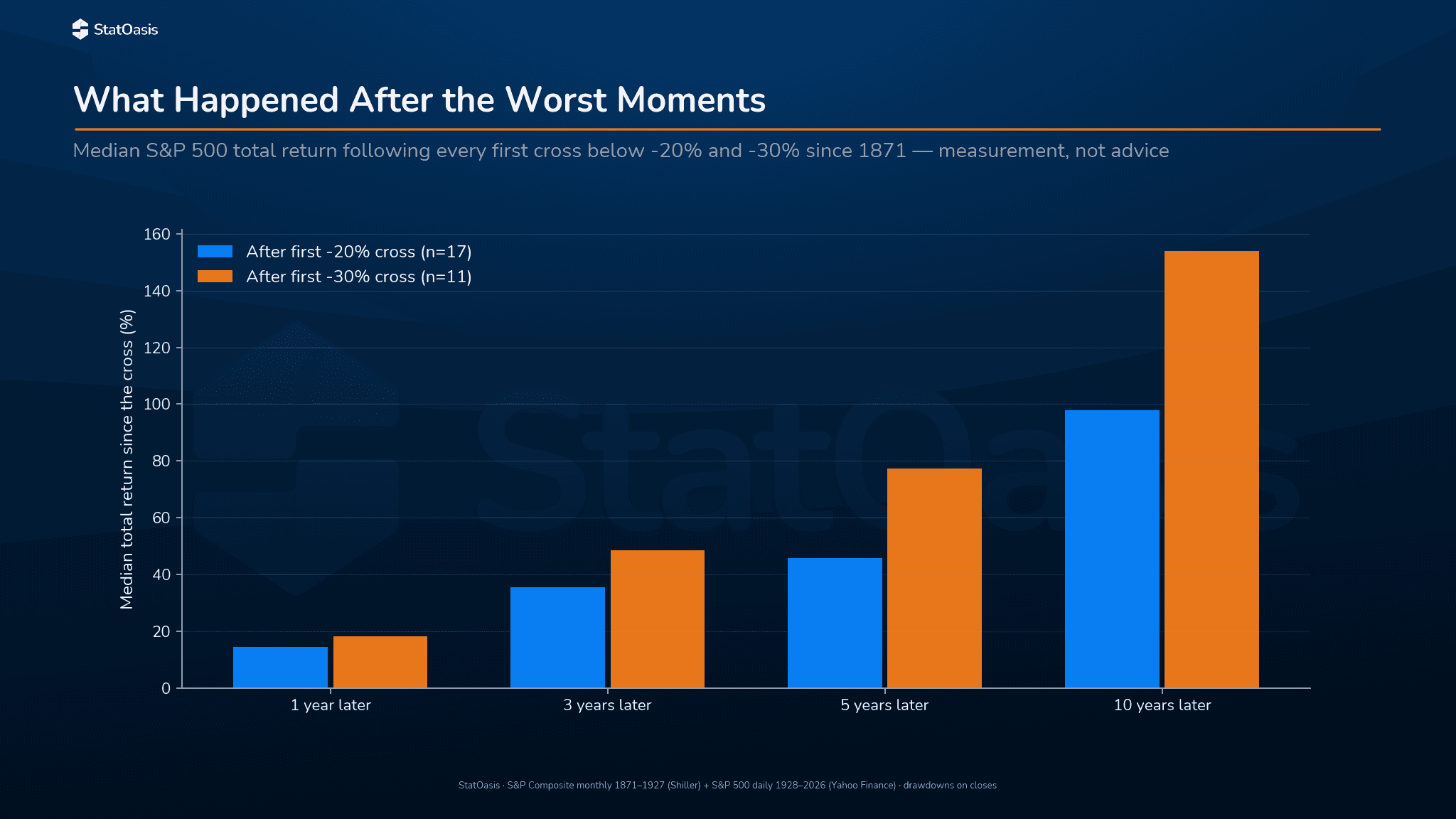

What happened after the worst moments

Here's a question with real money attached: the market has just crossed 20% down, the news is uniformly terrible, and you have cash. What did buying that moment look like, historically?

We found every first time each episode crossed 20% down (17 times since 1871) and 30% down (11 times), then measured total return (dividends reinvested) from that day forward.

After first crossing… | 1 year later (median) | 3 years | 5 years | 10 years |

|---|---|---|---|---|

−20% (17 times) | +14.5% | +35.5% | +45.7% | +97.8% |

−30% (11 times) | +18.1% | +48.5% | +77.4% | +153.9% |

What happened after the worst moments: median total return from every first −20% and −30% cross since 1871. Measurement, not advice. Source: StatOasis, computed from Shiller monthly + daily S&P 500 data.

The medians are strongly positive at every horizon, and deeper entry points did better: the median 10-year total return from a −30% cross was +153.9%, versus +97.8% from a −20% cross. The odds moved the same way. From a −20% cross, 70.6% of the 1-year outcomes were positive, 93.8% of 5-year outcomes, and 10 years out, all 15 completed cases were positive. From −30%: 72.7% positive at 1 year, and every completed 10-year case is positive.

Inflation-adjusted, the story softens but survives: the median real total return 10 years after a −20% cross was +60.1%, with 93.3% of cases positive.

Two honest qualifiers before anyone gets excited. First, these are medians around wide outcomes: the 1-year number was negative roughly three times out of ten, and buying the first 20% cross in 1929 meant riding down much further before any of those gains arrived. Second, "100% positive at 10 years" is a statement about 15 historical cases in one unusually successful country, not a law of nature. Section 11 is about exactly that.

The cost of panicking, computed

Every drawdown produces the same tug-of-war in an investor's head: this time it won't come back. So we priced the panic. The simulation is simple and deliberately unflattering to the seller: an investor holds the index, sells everything the day the episode first closes 20% down, and buys back in on the day the market recovers its old high — the moment "it's safe again." Their opponent simply holds. Dividends reinvested for both. The wealth math itself runs on monthly data: the crossing and recovery dates are each mapped to the following monthly total-return observation, so the dollar figures below are a monthly-resolution approximation of the day-based story just told.

Across the 17 episodes with a −20% cross and a completed recovery, the median result: the panic seller ends the episode with 70.9% of the holder's wealth. Sell scared, buy back comforted, and the typical single episode costs you about three dollars of every ten. Everything the market gained between the bottom and the old high happened while you were out.

The worst case was, of course, 1929: a seller who bailed at −20% and waited for the (price) recovery kept just 15.6% of what the holder had.

And if someone had repeated the panic-sell playbook at every one of the 17 opportunities since 1871? Compounding all 17 episodes together leaves 0.016% of the holder's wealth (about $2 of every $10,000). Treat that number as an illustration, not a forecast: no real person panic-sells identically for a century and a half. But the direction of the arithmetic is the point. The strategy of leaving during declines and returning at new highs systematically sells low and buys high, and it compounds against you every single time. Selling by rule instead of by fear is a different thing entirely - we tested one of the oldest examples in 40 in, 20 out: the hedge fund trend strategy still in use today.

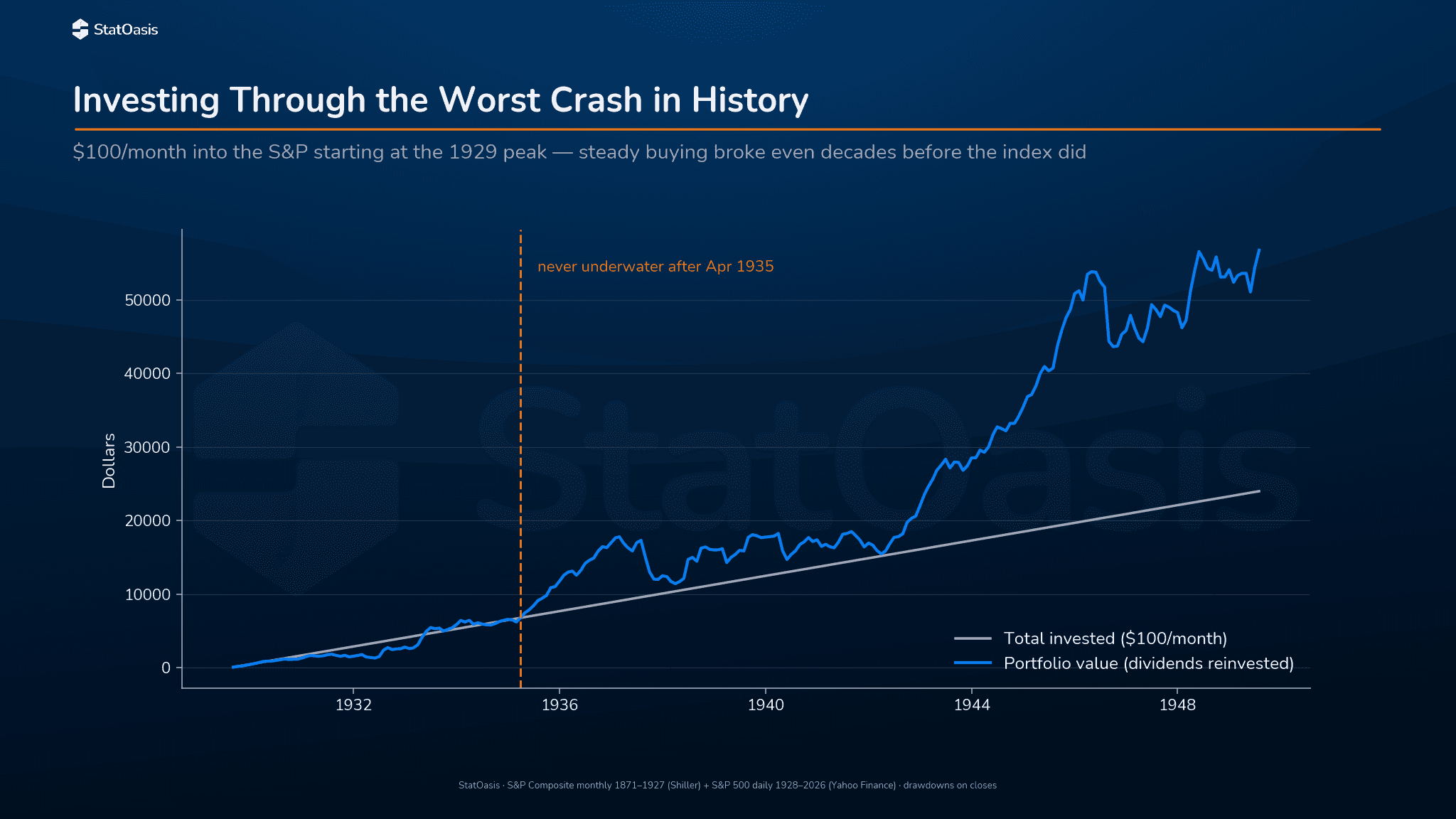

The mirror image is what buying through the decline looked like, so we ran the hardest version of that test in history: invest $100 every month, starting at the exact monthly peak in September 1929, straight through the Great Depression, dividends reinvested.

Investing through the worst crash in history: steady monthly buying was durably above water by April 1935, nearly two decades before the index price reclaimed its 1929 peak in September 1954. Source: StatOasis, computed from Shiller monthly data.

The result still surprises me, and I built the test. The steady buyer first touched break-even in March 1930, a blip during a bear-market rally that was quickly gone again. The durable answer: from April 1935 on, the plan was above water for good, while the market itself was still deep in the worst drawdown ever recorded. Adjusted for inflation, the durable break-even came in September 1942. The index price, remember, didn't reclaim its 1929 peak until September 1954. Every $100 invested during the collapse bought shares at 30, 50, even 80 percent off, and those cheap shares, plus their reinvested dividends, carried the whole plan back to even two decades before the index got there. The crash was the worst thing that ever happened to a 1929 lump-sum investor and, strange as it sounds, a gift to the one who kept buying. If you want the strategy comparison rather than the history, we've put steady buying head-to-head against timing rules in Dollar Cost Averaging vs Moving Averages.

Japan, the UK, and survivorship bias

Everything above has a hidden assumption baked in, and an honest study has to say it out loud: all of it is measured on the S&P 500, which is history's best-case major stock market. Since 1871, the United States has gone from recovering from a civil war to the largest economy on earth without losing a war at home, defaulting, or shutting its exchange for years. "The market always came back" is partly a fact about equities and partly a fact about picking the winner after the race.

Two sourced comparisons show what the same chart looks like elsewhere.

Japan. The Nikkei 225 closed at an all-time high of 38,915.87 on December 29, 1989. It did not close above that level again until February 22, 2024 — about 34.1 years underwater. An entire working career, from start to retirement, inside a single drawdown. That happened in the world's then-second-largest economy, not a frontier market.

The UK. The British market fell about 73% from its May 1972 peak to its December 1974 trough (Monevator; Wikipedia reports the same −73% for the FT 30), and per Wikipedia, it did not return to that nominal level until May 1987 — about 15.0 years underwater. The recovery then lasted only months before the October 1987 crash arrived.

The honest caveat: even the US worst case is mild next to Japan's 34-year drawdown. The S&P 500's history is the survivor's history. Source: StatOasis computed (US); nippon.com and Monevator/Wikipedia (Japan, UK).

So when this page says every S&P 500 drawdown recovered (and all 32 did), read it precisely. It means: in the single most successful market in modern history, declines of every size were eventually reclaimed, usually far faster than the folklore claims. It does not mean any one country's index, over any one investor's horizon, is guaranteed to come back. That distinction is an argument for global diversification, and it's the reason the forward-return tables in section 9 describe history rather than promise a floor. If you want the practical version of that argument, we've written a primer on tactical asset allocation - investing across asset classes without market predictions.

Key takeaways

Being underwater is the market's normal state: 82% of all months since 1871 were spent below a prior high, and only 18% at a new one (price basis). A 10% decline has arrived about every 4.9 years, a 20% bear about every 9.1.

Depth predicts duration. Median 10–20% declines resolved in about three months down and three back; 40%+ collapses took a median of 959 days down and 1,638 back. Recoveries have sped up: median 337 days since 1950, versus 1,112 before.

The 25-year Depression recovery is a price-only artifact. With dividends reinvested, it was 15.3 years; in real purchasing power, 7.2. The same math cuts the other way in inflationary eras: 1973 was 12.0 real years and 2000 was 12.7, and in real terms the 2000s were one continuous drawdown with no separate 2007 episode.

The worst moments were, historically, the best prices. Median total return 10 years after first crossing −20% was +97.8%; after −30%, +153.9%, with every completed 10-year case positive.

Panic had a price tag: the median −20% panic-seller who bought back at recovery kept 70.9% of the holder's wealth, and 1929's seller kept 15.6%. Meanwhile, $100/month started at the 1929 peak and was durably above water by April 1935.

All of this is the winner's history. Japan spent about 34.1 years underwater from 1989; the UK fell about 73% in 1972–74. The S&P's perfect recovery record describes the S&P, not a law of markets.

Frequently asked questions

What is the biggest S&P 500 drawdown in history?

The 1929–1932 collapse: −86.2% from the peak of September 16, 1929, to the trough of June 1, 1932, measured on daily closes. It is also the longest, at 25.0 years underwater on a price basis — though with dividends reinvested, the recovery took 15.3 years, and adjusted for inflation, 7.2.

How often does the S&P 500 fall 20% or more?

Seventeen times since 1871, or about once every 9.1 years on average. Declines of 10% or more happened 32 times (every 4.9 years on average), 30% or more eleven times (every 14.1 years), and 50% or more just twice.

How long does it take the S&P 500 to recover from a drawdown?

It scales with depth. Since 1871, declines of 10–20% took a median of 94 days to climb from trough back to the old high; 20–30% declines took 386 days; 30–40% took 639; and declines of 40% or more took 1,638 days. Recoveries have also accelerated: for 15%+ episodes, the median recovery is 337 days since 1950 versus 1,112 days before.

Is the S&P 500 usually at an all-time high?

No. Since 1871 the index was at a record close in only 18.0% of months (31.0% counting reinvested dividends). It spent 82% of months below a prior high and more than half of all months — 55.8% — in a drawdown of 10% or worse.

Does the stock market always recover from a crash?

The S&P 500 has, so far: all 32 episodes of 10%+ since 1871 eventually made new highs. But that is the record of history's most successful market. Japan's Nikkei 225 needed about 34.1 years to exceed its 1989 peak, and the UK market that fell about 73% in 1972–74 took roughly 15 years to reclaim its old nominal level. Recovery is a strong historical pattern, not a guarantee.

Disclaimer

All results in this article are derived from historical index data (Robert Shiller's S&P Composite dataset and daily S&P 500 closes) and do not represent actual trading results. The panic-cost and dollar-cost-averaging computations are hypothetical illustrations, calculated without taxes, fees, or transaction costs, which would change the outcomes. Past performance does not guarantee future results — including the S&P 500's historical record of recovering from every decline. This article is for educational and informational purposes only and does not constitute investment advice. StatOasis is not a registered investment advisor. Nothing here is a recommendation to buy or sell any security. Please consult a licensed financial professional before making any investment decision.

Transparency: StatOasis publishes a free newsletter and sells trading-education products. Our research is produced independently and is not altered to favor a sale.

Freshness: The data runs through 2026-07-02. We refresh this study when the underlying dataset is extended, and the "Last updated" date at the top reflects the last data point.

Written by Ali Casey, founder of StatOasis and AlgoChef, creator of ATM, with over 14 years of experience building systematic trading tools — building algorithmic strategies, testing ideas with data, and teaching traders how to build structured, portfolio-based trading workflows.

Whenever you're ready, here is how I can help you:

Algo Trading Masterclass

Unlock your path to financial freedom with our flagship course, StrategyQuant X's Algo Trading Masterclass. I share my extensive expertise, proven strategies, and practical workflows designed to set you on the course to becoming a successful trader.

StatOasis TAA Portfolios

Discover our specially curated portfolios for trading global liquid ETFs with just 15 minutes of your time each month. Based on hundreds of peer-reviewed whitepapers, our portfolios employ Tactical Asset Allocation and Factor Investing to maximize your returns

StatOasis Free Community

Join the ultimate trading hub to exchange ideas, pose questions, and engage in discussions with fellow traders. Our community is the perfect place to expand your trading network and knowledge.

The Algo Trader Newsletter

Stay informed with our newsletter, where I deliver exclusive tips and insights on investing, finance, and trading, helping you stay ahead in the markets.